Lambert Capital

Leading the Way in Property Development Finance and credit fund management

ARE YOU AN

INVESTOR

Are you a

BORROWER

Lambert Capital

Lambert Capital partners with experienced property developers and sophisticated investors to fund quality projects and realise superior risk-adjusted returns.

Lambert Capital focuses on assisting its many long-standing loyal clients, both borrowers and investors, via its proprietary Lambert Capital Property Credit Fund.

Find Out More about Lambert Capital

Lambert Capital’s Services

Borrowers

investors

Our Latest Insights

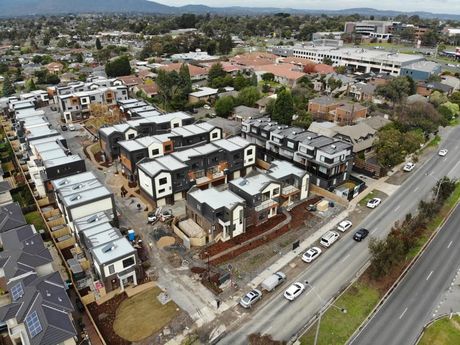

Confidence among Australian property developers has strengthened in recent months, with stabilising construction costs, stronger end-buyer demand and renewed activity in key markets helping turn sentiment around. The shift comes despite Australia’s construction sector ending the 2024-25 financial year on a soft note , with ABS building activity data showing dwelling commencements down 4.4% in the June quarter. Mark Greenberg, founder of non-bank lender Lambert Capital, said the rebound in sentiment has been noticeable since early 2025 as developers gain the confidence to progress projects that had been on hold. “We’re seeing increased enquiries and a more positive attitude from both developers and end buyers,” Greenberg said. “Developers who had paused projects are now feeling more confident as construction costs stabilise, allowing them to deliver products they can pre-sell, hold to sell post-construction or rent out for longer-term investment with greater certainty.” Cost Pressures Easing and Pipeline Staying Strong According to Cotality’s Cordell Construction Index, residential construction costs rose just 0.5% between the March and June 2025 quarters – half the pre-pandemic average of 1.0%. This slowdown suggests that the cost surge seen through recent years is finally settling, creating better conditions for project feasibility and funding. Even with fewer new starts, the national pipeline remains elevated, with more than 223,000 dwellings still under construction in the June quarter. For mortgage brokers, the easing in cost inflation and sustained pipeline provide ongoing financing and settlement opportunities as projects move toward completion. Completions dipped 6.5% to 40,524 dwellings, while the total value of building work done eased 0.3% to $38.9 billion – reinforcing the need for faster approvals and productivity reforms to lift future supply. Buyer Demand Returning in Key Markets Improved housing affordability , interest-rate cuts , and first-home-buyer incentives are drawing more purchasers back into the market. The Housing Industry Association reported that new-home sales reached a three-year high in August 2025, a positive sign for construction lenders and brokers supporting developer clients. “We’re particularly seeing renewed demand in more affordable markets like Victoria and Tasmania,” Greenberg said. He said stronger enquiry levels are especially encouraging given the patchy national construction data. “The market is starting to find its balance – while starts are lower, the appetite to buy or build has clearly improved,” Greenberg said. Investors Target Undervalued States Cotality’s Home Value Index shows the strongest price growth over the past five years in Perth (+82.7%), Adelaide (+77.2%), and Brisbane (+80.1%). By contrast, Melbourne rose 17.5% and Hobart 29.5%. This widening gap has positioned Victoria and Tasmania as comparatively undervalued, attracting investors and owner-occupiers searching for better value. “In some cases, we’ve seen residual stock from earlier subdivision stages start selling much faster – what might have taken 10 months to sell is now moving in 10 weeks,” Greenberg said. He added that faster sales have encouraged developers to progress to new stages, noting that “we’re still nowhere near oversupply – it’s simply catching up.” Sustainable Growth Ahead While markets have tempered expectations for aggressive rate cuts, Greenberg said the moderation is healthy for the sector. “The developers moving forward now tend to be experienced operators who can deliver quality at the right price – not speculative players chasing short-term gains.” Industry leaders have echoed that confidence but warn that continued regulatory reform is essential to meet housing targets. Master Builders Australia CEO Denita Wawn said accelerating approvals, addressing skill shortages, and supporting private investment will give industry the certainty to get projects moving. Greenberg expects stronger construction activity in 2026 as developers align product pricing with renewed demand and affordability. “It’s encouraging to see developers start building again,” he said. “After years of hesitation, the market finally feels like it’s moving in the right direction.”

The Lambert Capital Property Credit Fund recently settled a tailored construction facility for a new client undertaking the development of 27 warehouses in the developing corridor between Sydney and Newcastle.

The Lambert Capital Property Credit Fund recently settled a loan facility for a returning developer client who needed to refinance existing land debt and secure construction funding in the growing location of Coral Cove, Queensland. Project Overview Location : Coral Cove, QLD. Loan Amount : $25M Loan Type : Re-Finance & Construction Benefits to Developer Settlement in Less Than 3 Weeks. Tranche-Style Tailored Funding Solution. Reduced Upfront Costs. Regional Location.